Is International Finally Ready to Shine?

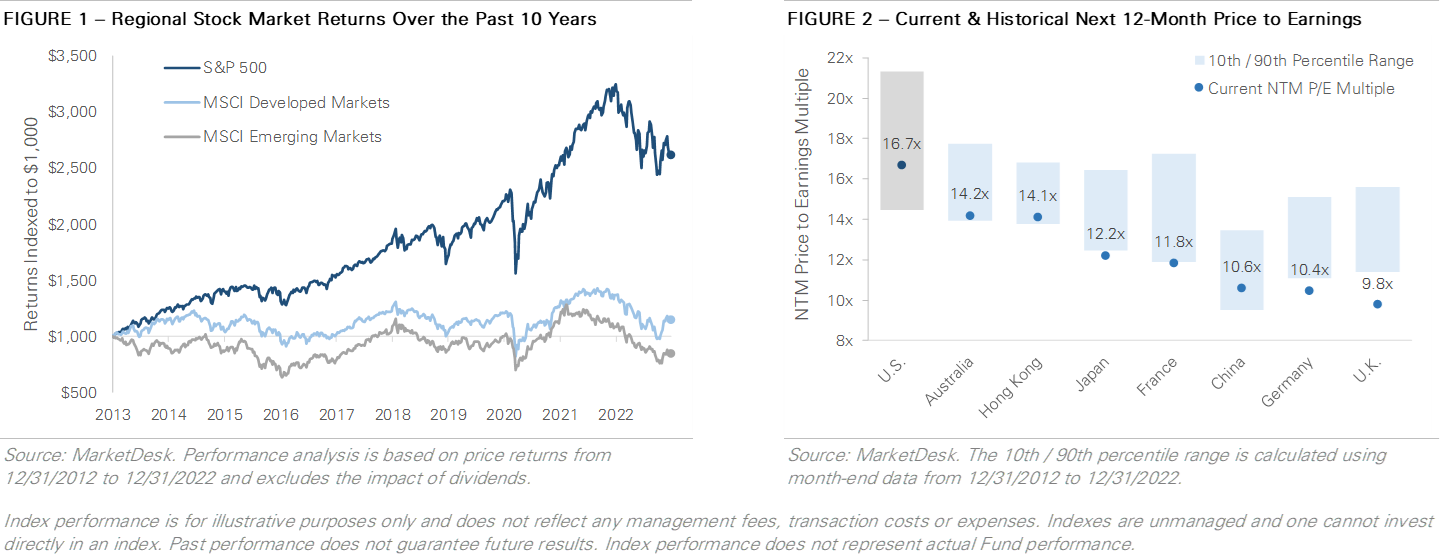

For comparison, the same $1,000 investment in the MSCI Developed Market Index returned only $1,142, while a $1,000 investment in the MSCI Emerging Market Index posted a loss and returned $842.

Looking back at the last decade, investment analysts attribute the outperformance of U.S. stocks to several factors. One major contributing factor is the composition of the S&P 500 Index, which is heavily weighted towards technology and other growth-oriented stocks such as Apple, Amazon, Microsoft, Google, and Tesla.

This high concentration of technology stocks is not found anywhere else around the world, and as the group outperformed, so did the broader U.S. stock market. Additionally, the U.S. dollar strengthened by approximately 30% over the last decade, which decreased the value of foreign investments when translated back into U.S. dollars.

These two catalysts benefitted U.S. stocks while acting as a headwind for international stocks.

Today international stocks currently trade at more attractive valuations than U.S. stocks after a decade of underperformance. As illustrated in Figure 2, U.S. stocks trade at a higher next 12-month price-to-earnings multiple than international stocks. In addition, U.S. stocks trade more expensive against their historical valuation range, as evidenced by the 10th to 90th percentile range of historical price-to-earnings multiples.

Given the current valuation backdrop, growth stocks’ underperformance in 2022, and recent U.S. dollar weakness, international stocks may become more of a focus for investors in 2023.